Knowing Payment Gateway Doesn’t Have To Be Hard

by 20/09/2019 15:240

According to one GoodFirms e-commerce app survey, 52.3% of the participants say Payment Gateway is the prime factor affecting the cost of e-commerce app development. This insight is valuable for entrepreneurs who are planning to launch an app for their online business, especially an e-commerce business.

They can drive more business if they make this app user-friendly and provide paymnt options preferred by the customers. But not unless they have an idea of how the entire process works. Eventually, the business owner would be handling the customers’ sensitive financial data.

What is the Payment Gateway and how it Works?

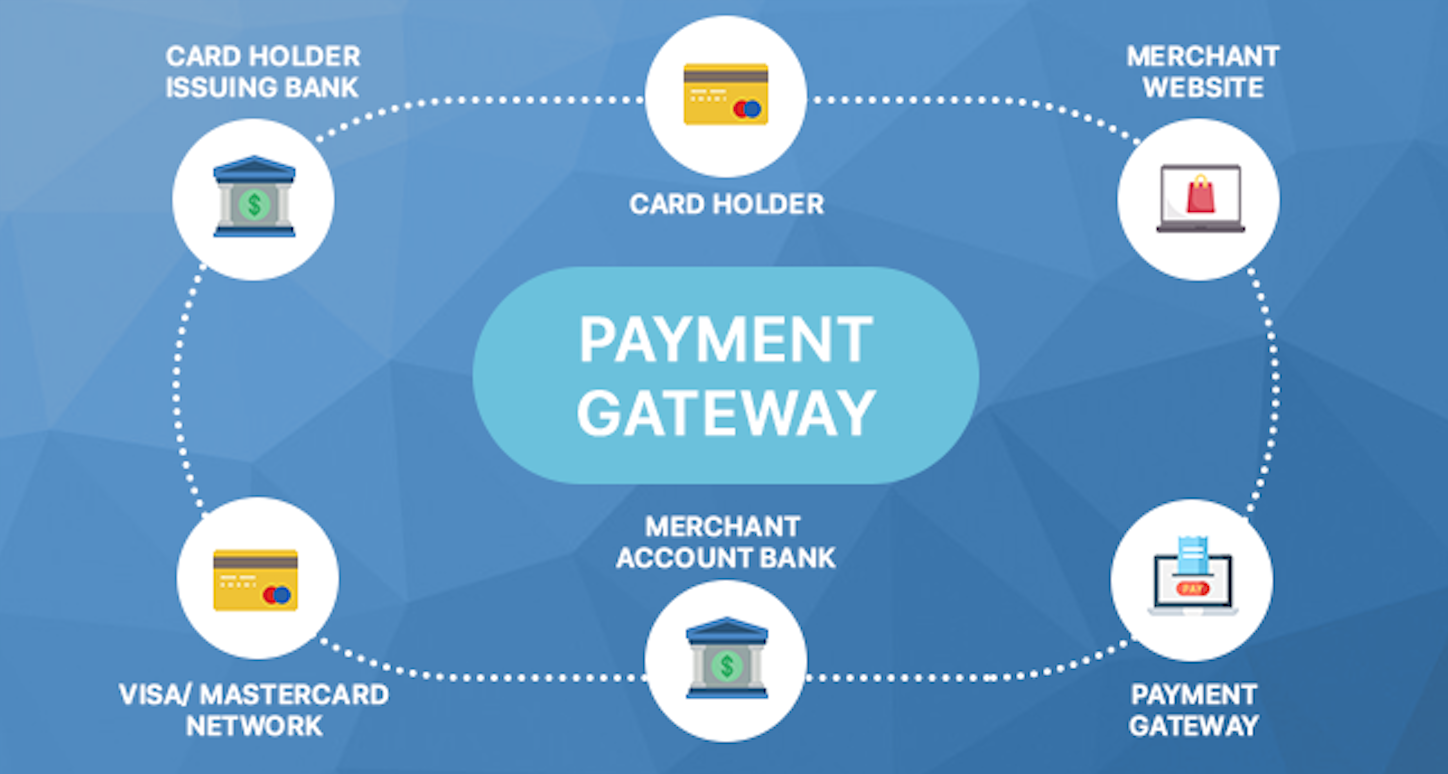

In simple words, a payment gateway is a third-party tool that exists between merchant and customer to securely process the online transaction. It’s a service that authorizes credit card transactions during online shopping and mostly used by e-commerce sites.

Unlike swiping credit cards in a physical store, when the customer buys product on the internet, the payment gateway authenticates the customer’s digital credentials before forwarding information about the transaction to the payment processor.

Some payment gateway comes bundled with shopping cart software while other integrates with e-commerce software.

How Payment Gateway works?

The entire payment gateway process revolves around four key players— customer, merchant, acquiring bank, and issuing bank. The latter two terminologies “acquiring bank” and “issuing bank” require little more stress as it often validates the process.

- The acquiring bank is the host bank of the merchant

- The issuing bank is the host bank of the customer

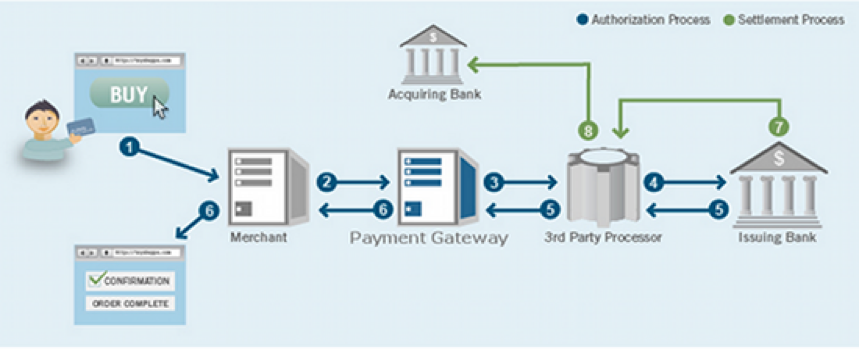

Now let see how the entire payment gateway process takes place.

Below steps are explained in reference to the above image,

- Buyer clicks on BUY Button on the merchant’s website and initiates the payment process

- Buyers card information is collected on the merchant server and sent to the payment gateway

- Payment gateway sends transaction information to the payment processor used by the merchant’s acquiring bank. The acquiring bank cross-verifies the customer’s card Networks (Visa, Master Card, etc.)

- Once the card network is confirmed (Visa, Master card, etc.) the third party processor routes the request to the corresponding bank that issued the card or the issuing bank (buyers bank)

- The issuing bank receives the authorization request, verifies the request, and sends a response back to the processor. Payment Processor forwards this information to the Payment Gateway

- Payment Gateway forwards it to the merchant website and confirms order completion

- In the end, the payment gateway performs a process called Settling. In this process, your bank verifies the data and money from sales is deposited into your account.

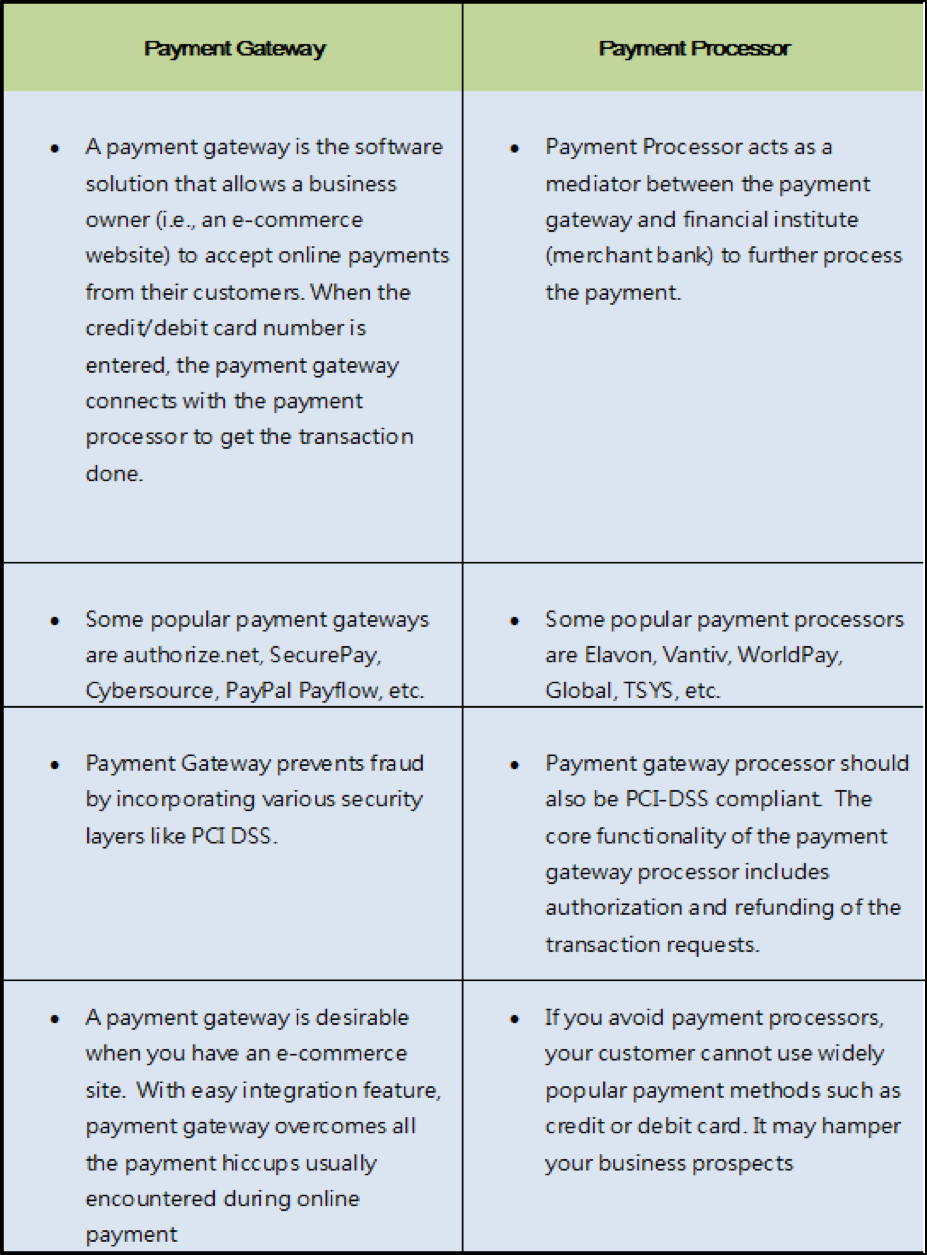

Difference between Payment Gateway Vs. Payment Processor

Since now you know how it works, let’s check out how safe the Payment Gateway is. Without the customer and card physically present, authenticating an online transaction is a sensitive process. It is, therefore, necessary to have a standard security protocol to protect customer’s confidential data.

Here are the key parameters to check your Payment Gateway Security.

- SSL protocol (HTTPs): All transactions should be secured with SSL protocol. To verify it, check the website address has “https” in it.

- Tokenization: Make sure the customer data should be transmitted in an encrypted form (token Ids). When token replaces the live data it restricts the unauthorized access to sensitive data.

- PCI DSS (Payment Card Industry Data Security Standard): It is referred as a list of practices for merchants accepting payment to comply. By meeting PCI DSS compliance, businesses can protect cardholder information from being stolen and improves the security of card transactions. Use a firewall on your network and PCs.

- 3D secure: To detect and stop fraud, a consumer should choose a payment gateway that provides an extra layer of security known as 3D secure. At the time of every transaction, the password is verified with the help of a site that supports the scheme

- Anti-fraud tools: There are tools that highlight the field of payment form with the word “suspicious” when someone tries to buy something with fake credit cards or a fake account.

In summary,

E-commerce being the fastest growing sector, the payment system needs to be quick and smooth. But at the same time it is essential to see what payment services are suitable for your customers and whether the service is upgraded to the latest security compliances. Other dimensions business owner should consider checking before finalizing the gateway system are the payment processing charge per transaction and monthly fees.

Author Bio- Jimmy Johnson is an avid reader and full-time writer for GoodFirms. His fascination for technology was one-dimensional until he discovers how Robotic Process Automation and Cloud Computing can enhance business services. Since then, he scouts on many such exciting technologies that empower businesses beyond expectation.

Related posts

Technology / by - ago

Dr Melvin Rabin: How Artificial Intelligence Is Transforming Modern Medicine

Dr Melvin Rabin is a retired clinical psychologist who spent nearly five decades treating patients at his practice in Needham, Massachusetts. At Rabin Associates, he addressed a wide range of…

Technology / by - ago

Yamaha R15: The Perfect Entry-Level Supersport for Indian Riders

Choosing a first supersport motorcycle can be hard for many riders. New riders usually look for a bike that looks sporty, has modern technology, and is easy to handle. The…

Technology / by - ago

How to Upgrade Your Front Porch to a Cosy Retreat

Your front porch is the first impression of your home, yet it is often overlooked as a space that can be both functional and inviting. With a few thoughtful upgrades,…

Technology / by - ago

Behind The Security Curtain: How QQWIN4D Ensures Safe Transactions Every Single Time

Do you want to know how QQWIN4D keeps each transaction safe in a simple and steady way? Many users think about this before they add funds, check account details, or…